Financial Crimes: The Con Artists of Wall Street

From Ponzi's 1920 Boston scheme to LIBOR manipulation by global banks in 2012 — six cases that reveal how financial crime exploits information asymmetry and why prosecutions represent a fraction of the activity.

Financial Crimes: The Con Artists of Wall Street

Financial crime in America runs on one durable mechanism: someone with access to financial markets exploits an information asymmetry, a structural vulnerability, or a position of trust to extract value from people who don’t know what’s happening. The six cases in this series — spanning from Charles Ponzi’s 1920 Boston scheme to the global LIBOR manipulation that ran through 2012 — involve different instruments and different victims. The pattern under each of them is the same.

In This Series

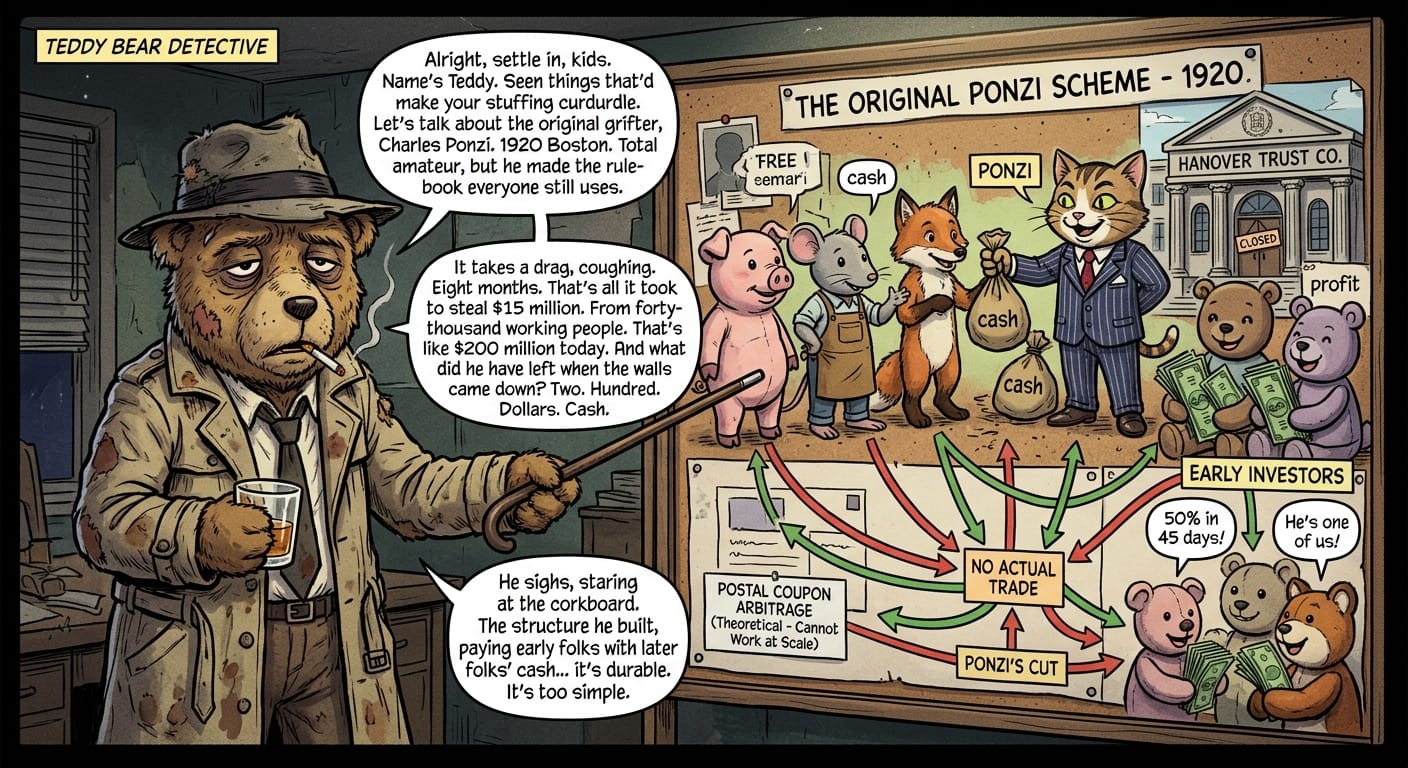

- Charles Ponzi: The Man Who Invented the Scheme — The 1920 postal coupon fraud that collected $15 million from 40,000 Boston investors in eight months and gave every subsequent scheme its name.

- Bernie Madoff: The Biggest Ponzi Scheme in History — The NASDAQ chairman who ran a $64.8 billion fraud for at least 17 years while the SEC received multiple credible warnings and did nothing.

- Michael Milken and Junk Bonds: The Man Who Corrupted Finance — The Drexel Burnham Lambert architect who paid $600 million in fines, served 22 months, and later received a presidential pardon.

- Jordan Belfort: The Real Wolf of Wall Street — The Stratton Oakmont founder who defrauded retail investors of $200 million, paid back less than $12 million in restitution, and sold the story for a movie deal.

- Insider Trading: Wall Street’s Most Lucrative Crime — Why prosecutions represent a fraction of the activity, and what Boesky, Rajaratnam, and SAC Capital reveal about who gets caught.

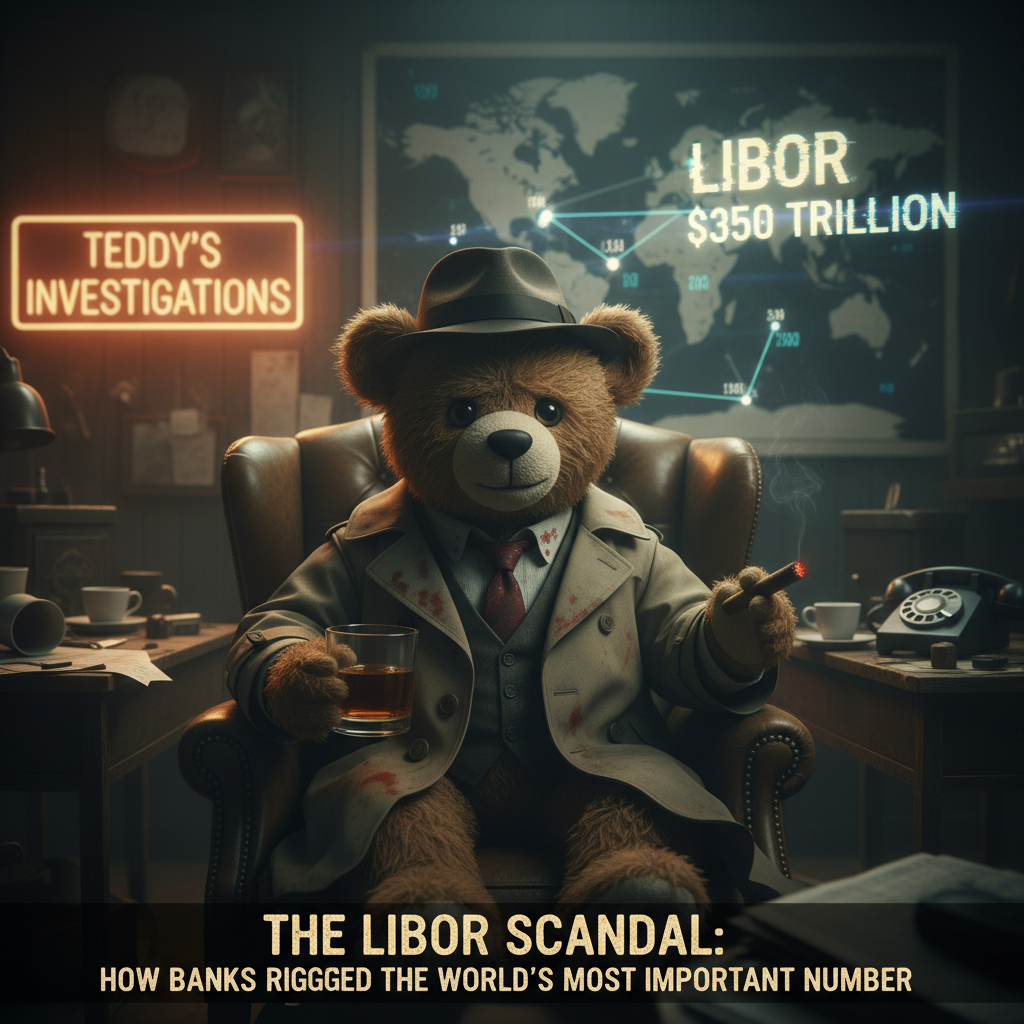

- The LIBOR Scandal: How Banks Rigged the World’s Most Important Number — Banks falsified the benchmark rate for $350 trillion in global contracts over nearly a decade, generating $9 billion in fines and almost no individual criminal convictions.

The Information Asymmetry That Makes It All Possible

Every financial crime depends on one party knowing something the other doesn’t. Charles Ponzi knew he wasn’t actually trading postal coupons; his investors didn’t. Bernie Madoff knew he wasn’t executing any trades; his investors didn’t. Ivan Boesky knew which companies were merger targets before the announcements; the market didn’t. The LIBOR panel banks knew what rate they were actually paying to borrow; the $350 trillion in contracts that referenced their submitted rates didn’t.

The asymmetry is structural. Financial markets are complex enough that most participants — including institutional investors — cannot fully verify what they’re being told. This is why auditors, regulators, and disclosure requirements exist: to compensate for the verification gap. Every case in this series represents a failure of one or more of those compensating mechanisms.

Why Ponzi Schemes Can’t Stop Once They Start

The most striking feature of Ponzi schemes is that they cannot stop voluntarily. Once the fraud begins, the operator is trapped: to stop paying returns to existing investors is to expose the fraud. So new investors must continuously be recruited. The scheme must grow until it can’t, at which point it collapses. Ponzi’s scheme lasted eight months; Madoff’s lasted at minimum 17 years. The difference in duration reflects the difference in the operator’s social capital, institutional credibility, and ability to manage the flow of information about the underlying accounts.^1^

Milken’s junk bond network and the LIBOR manipulation are structurally different — they’re not escalating Ponzi structures but ongoing extraction — but they share the same terminal dynamic: they continue until external investigation stops them, because the people running them have no incentive to stop voluntarily.

The Prosecution Gap Is Structural, Not Accidental

The cases that resulted in convictions are a fraction of the activity they represent. Markopolos documented the mathematical impossibility of Madoff’s returns in 2005 and the SEC did nothing. Academic studies consistently find abnormal trading before major announcements at rates that vastly exceed the SEC’s insider trading prosecution rate. The LIBOR manipulation continued for nearly a decade before regulators acted, despite being documented in internal communications that should have been visible to anyone looking.

Jordan Belfort paid back less than $12 million of $110.4 million in restitution before becoming a motivational speaker. Milken received a presidential pardon after serving 22 months. SAC Capital paid $1.8 billion while its principal faced no criminal charges. The pattern across these cases is that financial consequences for perpetrators are real but partial, criminal consequences are inconsistent, and victims are rarely made whole.^2^

Who Gets Labeled a Criminal Tracks Closely With Who Can Hire the Best Lawyers

The legal treatment of financial crime in the United States is heavily influenced by who can hire the best lawyers and whether investigators can find cooperating witnesses. The pump-and-dump operators targeting retail investors in the 1990s — Belfort’s Stratton Oakmont, its many imitators — got prosecuted vigorously. The LIBOR manipulation by major global banks took years to prosecute, resulted in institutional fines rather than widespread individual convictions, and saw multiple individual criminal convictions reversed on appeal. The mechanisms are not equivalent, but the difference in enforcement energy tracks closely with the power and resources of the institutions involved.

The financial crimes in this series were constrained, eventually, by a combination of prosecutorial action, market collapse, and regulatory reform. The reforms are real — Sarbanes-Oxley, Dodd-Frank whistleblower provisions, LIBOR replacement with transaction-based benchmarks. But they address specific vulnerabilities that have already been exploited. The underlying conditions persist: complex instruments that most investors can’t evaluate, compensation structures that reward short-term gains, regulatory agencies with fewer resources than the institutions they regulate. The con artists change. The structure of the con doesn’t. The same dynamic runs through the corporate fraud series — from Enron’s hidden debt to FTX’s missing customer deposits — because the oversight failures are the same.

─────────

Sources:

- Henriques, Diana B. The Wizard of Lies. Times Books, 2011.

- Markopolos, Harry. No One Would Listen. Wiley, 2010.

- Stewart, James B. Den of Thieves. Simon & Schuster, 1991.

- Vaughan, Liam, and Gavin Finch. The Fix. Wiley, 2017.

- Kolhatkar, Sheelah. Black Edge. Random House, 2017.

The Series