Enron: The Company That Lied Until It Died

Enron hid $1 billion in debt through off-book partnerships while 20,000 employees sat on $1.2 billion in pension savings they couldn't sell. How the largest accounting fraud of 2001 actually worked.

Enron: The Company That Lied Until It Died

Enron corporate fraud didn’t start as theft — it started as a real energy trading business that ran out of honest options. When losses mounted faster than they could be disclosed, executives built an elaborate system to hide $1 billion in debt and inflate earnings by hundreds of millions, while 20,000 employees sat on $1.2 billion in pension savings they couldn’t touch. The lie held for years because everyone positioned to catch it had a financial reason to look away.

Part of Corporate Fraud — ← Back to series hub

How Enron Became a Trading Company

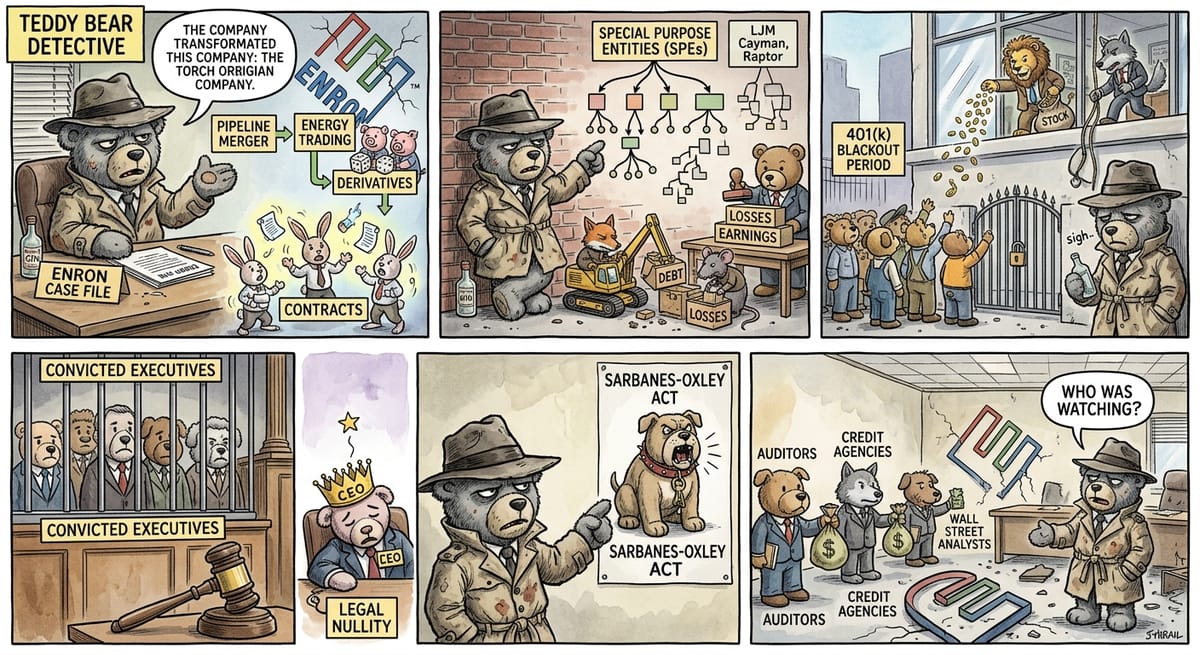

Enron began as a natural gas pipeline company formed in 1985 from the merger of Houston Natural Gas and InterNorth. Under CEO Kenneth Lay and later President Jeffrey Skilling, it reinvented itself as an energy trading company — a middleman that bought and sold electricity, natural gas, broadband capacity, and eventually weather derivatives and other exotic financial instruments.^1^

By 2001, Enron was reporting $111 billion in annual revenues, ranking it seventh on the Fortune 500. Skilling had assembled a team of traders and financial engineers who believed they had found a smarter way to run an energy company: don’t own physical assets, trade contracts. The strategy generated real profits in the mid-1990s, but the company’s ambitions outpaced the underlying business. When trading positions went bad or new ventures failed, the losses had to go somewhere. They went off the books.

Why Did Enron’s Auditors Miss $1 Billion in Hidden Debt?

Chief Financial Officer Andrew Fastow engineered a network of special purpose entities — partnerships with names like LJM Cayman and Raptor — that served one primary purpose: absorb Enron’s losses and debt so they wouldn’t appear on Enron’s consolidated financial statements. Under accounting rules at the time, if an outside investor held at least 3% of an entity, Enron didn’t have to consolidate it. Fastow found outside investors willing to meet that threshold, often because Enron itself guaranteed their returns.^1^

Between 1997 and 2001, Enron used these arrangements to hide approximately $1 billion in debt and inflate earnings by hundreds of millions of dollars. Fastow personally collected at least $30 million in management fees from the partnerships he ran — transactions the board’s audit committee had approved without grasping their full scope.

The accounting firm Arthur Andersen signed off on all of it. Andersen earned $52 million from Enron in 2000 alone — $25 million in audit fees and $27 million in consulting fees.^2^ The financial incentive to keep the client happy was enormous. When federal investigators began closing in, Andersen employees shredded thousands of pages of Enron-related documents at the Houston office. The firm was convicted of obstruction of justice in 2002 and effectively ceased to exist, eliminating one of the five largest accounting firms in the world.

The Workers Who Couldn’t Sell Their Stock

The people who actually got hurt were people like Charles Prestwood, a 63-year-old Enron worker who had spent 33 years with the company. When Enron’s stock collapsed, he lost $1.3 million in retirement savings. Employees had been prohibited from selling Enron stock from their 401(k) plans during an administrative blackout period in October and November 2001, while executives had no such restrictions and were actively unloading shares.

Linda Lay, the CEO’s wife, went on the Today show the morning after the December 2001 bankruptcy filing to describe how hard the family had it. Ken Lay had sold $70 million in Enron stock back to the company in the preceding year, taking company loans to fund the sales.

Investors outside the company had also been misled. Wall Street analysts — many with conflicts of interest through investment banking relationships — kept Enron stock rated as a buy into the fall of 2001. Sherron Watkins, an Enron vice president, had warned Kenneth Lay in August 2001 that the company’s accounting structures were fraudulent.^2^ Her memo became one of the most damning documents of the scandal. The company continued lying for another four months.

The Sentences That Followed

Jeffrey Skilling was convicted in 2006 on 19 counts of fraud and conspiracy and sentenced to 24 years in federal prison.^3^ Andrew Fastow pleaded guilty in 2004 to two counts of conspiracy and received a six-year sentence. Kenneth Lay was convicted on six counts of fraud and conspiracy in May 2006, but died of a heart attack in July 2006 before sentencing — legally vacating his conviction under a doctrine that treats death before appeal as a nullity.

Twenty other executives were convicted or pleaded guilty. The investigation, led by the Enron Task Force within the Department of Justice, was one of the most concentrated prosecutorial efforts against corporate fraud in American history.

Congress responded with the Sarbanes-Oxley Act of 2002, which required CEOs and CFOs to personally certify the accuracy of financial statements, increased criminal penalties for securities fraud, and created new protections for corporate whistleblowers.^3^ The law passed 99-0 in the Senate and 423-3 in the House.

Every Watchdog Was Being Paid by the Dog

Enron worked because of failure at every layer of oversight. The board of directors — which included members with PhDs in accounting and finance — approved the special purpose entities without demanding to understand them. The auditors collected their fees and asked no hard questions. Credit rating agencies maintained investment-grade ratings on Enron debt until four days before the bankruptcy filing, by which point the company had already been revealed as insolvent. Analysts at major investment banks who rated the stock a buy had corporate clients who wanted to do business with Enron.

The pattern Enron established was repeated almost immediately: the same era produced WorldCom, Tyco, HealthSouth, Global Crossing, and Adelphia — a cluster of frauds suggesting Enron wasn’t an aberration but a visible expression of something systemic. On the financial crimes side, Bernie Madoff was running a parallel lie through the same period, built on the same institutional silence.

Enron’s collapse produced real reform. Sarbanes-Oxley imposed genuine accountability on corporate officers — a change that also shaped how later scandals like the Theranos fraud were eventually prosecuted. But the broader culture of financial engineering and creative accounting didn’t disappear with Arthur Andersen. The question Enron left behind wasn’t just “how did this happen” but “who was watching” — and the answer, uncomfortably, was almost no one.

─────────

Sources:

- McLean, Bethany, and Peter Elkind. The Smartest Guys in the Room: The Amazing Rise and Scandalous Fall of Enron. Portfolio, 2003.

- United States Senate Permanent Subcommittee on Investigations. The Role of the Board of Directors in Enron’s Collapse. U.S. Government Printing Office, 2002.

- Eichenwald, Kurt. Conspiracy of Fools: A True Story. Broadway Books, 2005.

- Fox, Loren. Enron: The Rise and Fall. Wiley, 2003.