Charles Ponzi: The Man Who Invented the Scheme

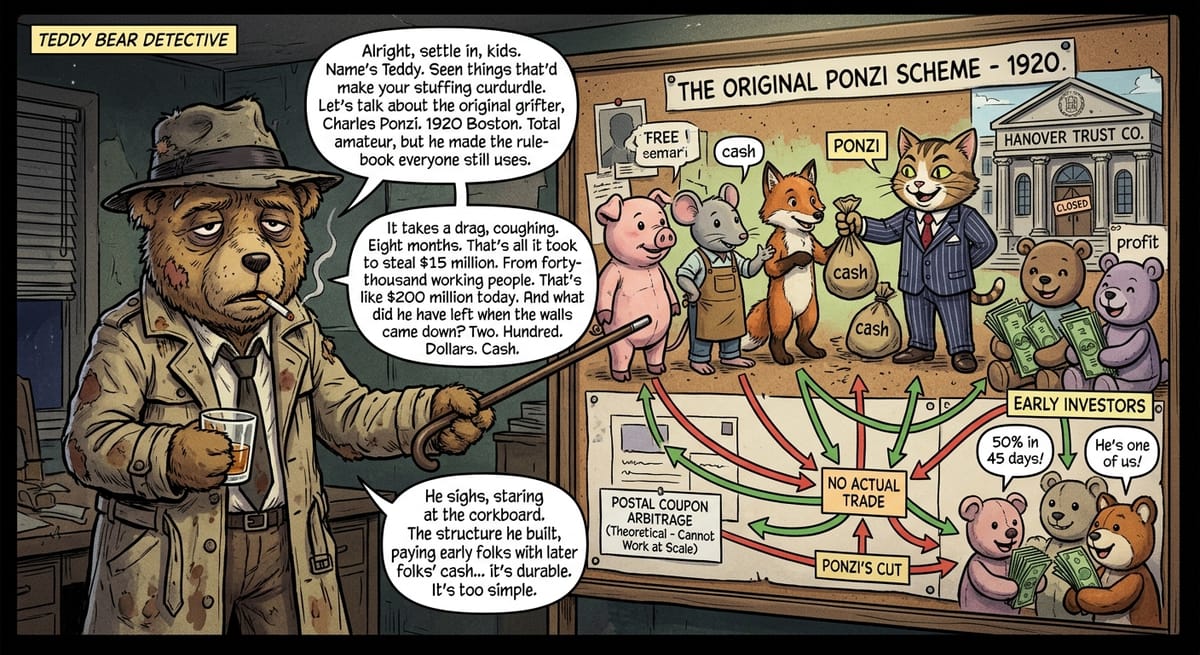

In 1920 Charles Ponzi collected $15 million from 40,000 Boston investors promising 50% returns in 45 days on a postal arbitrage that couldn't work at any real scale. He had $200 left when it collapsed.

Charles Ponzi: The Man Who Invented the Scheme

Charles Ponzi didn’t invent financial fraud, but in eight months in 1920 he ran the first Ponzi scheme at a scale that made his name permanent. He collected approximately $15 million from roughly 40,000 investors in the Boston area — equivalent to over $200 million today — promising 50% returns in 45 days on a postal coupon arbitrage that couldn’t work at any meaningful volume. When the scheme collapsed in August 1920, he had about $200 in cash on hand. The structure he ran — paying early investors with money from later ones — has been replicated thousands of times since, up to and including Bernie Madoff’s $64.8 billion operation eighty years later.

Part of Financial Crimes — ← Back to series hub

Carlo Ponzi Arrived in America with $2.50

Carlo Pietro Giovanni Guglielmo Tebaldo Ponzi arrived in the United States from Italy in November 1903 having spent most of his travel money gambling on the ship crossing. He spent the next 15 years drifting — working as a waiter, a storekeeper, a bank runner — with a series of convictions for fraud and forgery along the way, including time in a Canadian prison for signing someone else’s name to a check and a federal conviction for smuggling Italian immigrants across the border from Canada.

By 1919 he was living in Boston with a wife, Rose, and working as a clerk. He stumbled onto the idea that would make him famous by accident while reading a piece of mail from abroad.

The Arbitrage That Couldn’t Work at Scale

The underlying concept Ponzi pitched was international reply coupons — certificates that could be purchased in one country and redeemed for postage stamps in another. Because of post-World War I currency fluctuations, these coupons could theoretically be bought cheaply in European countries where currencies had collapsed and redeemed for more valuable American postage. Ponzi claimed he had set up a network of agents purchasing these coupons in bulk in Europe and converting them to profit in the United States.^1^

The arbitrage was real in concept but impossible in practice at scale: the entire global supply of international reply coupons at the time of his operation amounted to approximately 27,000 — nowhere near enough to generate the returns he was promising. He was not actually trading coupons. He was collecting money from new investors and paying old investors, with a cut going to himself and the agents he recruited on commission.

The scheme worked because the early investors got paid exactly as promised. Word spread through Boston’s Italian-American immigrant community — people who trusted one of their own — and then through the broader city. Ponzi rented office space at 27 School Street, hired staff, opened branches across New England, bought a mansion in Lexington, Massachusetts, and became a local celebrity.^1^

How the Boston Post Took It Down

The Boston Post began asking questions in July 1920, after financial analyst Clarence Barron pointed out the mathematical impossibility of the coupon arbitrage strategy. Ponzi sued the Post for a story he considered defamatory, which only attracted more attention. Bank runs on his offices began. Massachusetts regulators and federal postal inspectors launched simultaneous investigations.

On August 10, 1920, the Post revealed that Ponzi had a prior criminal record, including the Canadian forgery conviction. The disclosure triggered a complete bank run. William McMasters, a publicist Ponzi had hired, sold his account of the operation to the Post, estimating Ponzi was $2 million short of what he owed investors. Federal investigators eventually concluded the shortfall was closer to $7 million.^2^

Ponzi pleaded guilty to federal mail fraud and was sentenced to five years, of which he served three and a half. Massachusetts tried him on state charges; after a failed attempt to flee to Italy, he was convicted and served additional time. He was deported to Italy in 1934.

What the 40,000 Investors Actually Got Back

The 40,000 investors who didn’t get out in time received approximately 37 cents on the dollar after liquidation. Among them were small investors — laborers, domestic workers, shop owners — who had entrusted Ponzi with savings accumulated over years. One woman had borrowed against her home to invest. The Hanover Trust Company, a Boston bank in which Ponzi had purchased a controlling interest, collapsed as a result of the fraud, wiping out its ordinary depositors. Five other Boston banks with exposure to Ponzi-related deposits either collapsed or were significantly destabilized.^3^

Ponzi died in January 1949 in Rio de Janeiro, having spent his final years working as an Alitalia agent in Brazil. He left $75 in cash and a set of forged documents.

The Scheme’s Structural Durability

Ponzi’s conviction established criminal liability for scheme operators, but not a mechanism for catching them early. The SEC, created in 1934 partly in response to financial fraud patterns of the 1920s, received multiple credible complaints about Madoff’s operation and took no action for decades. The gap between Ponzi’s collapse and Madoff’s was 88 years and roughly $17 billion in direct losses.

The scheme’s power is its simplicity. It doesn’t require sophisticated technology, specialized knowledge, or complicit institutions — only the willingness to take money from people who trust you and give some of it to people who came before them. The same structural conditions that made it work in Boston in 1920 — the promise of extraordinary returns, the social trust of tight-knit communities, the inaccessibility of financial verification for ordinary investors — recur in every version of the scheme that followed. Understanding Ponzi means understanding why insider trading and LIBOR manipulation persist despite prosecution: the information gap between those who run the system and those who trust it is durable.

─────────

Sources:

- Zuckoff, Mitchell. Ponzi’s Scheme: The True Story of a Financial Legend. Random House, 2005.

- Dunn, Donald H. Ponzi! The Incredible True Story of the King of Financial Cons. Broadway Books, 2004.

- Ponzi, Charles. The Rise of Mr. Ponzi. Inkwell Publishers, 1936.

- Sobel, Robert. The Big Board: A History of the New York Stock Market. Free Press, 1965.